Five Advantages to Owning a Home

Your home is your castle, but there are also many financial advantages of owning a home. Here are five ways that owning can be better than renting.

1. As a Hedge Against Inflation

Your rent will go up on a regular basis, while your payment on a 30-year fixed mortgage will always remain the same.

Let’s say your monthly rent is $1,800. Assuming inflation (your rent increase) is 3 percent, in five years your monthly rent will be $2,026. By then, you will have paid about $115,000 of your landlord’s mortgage.

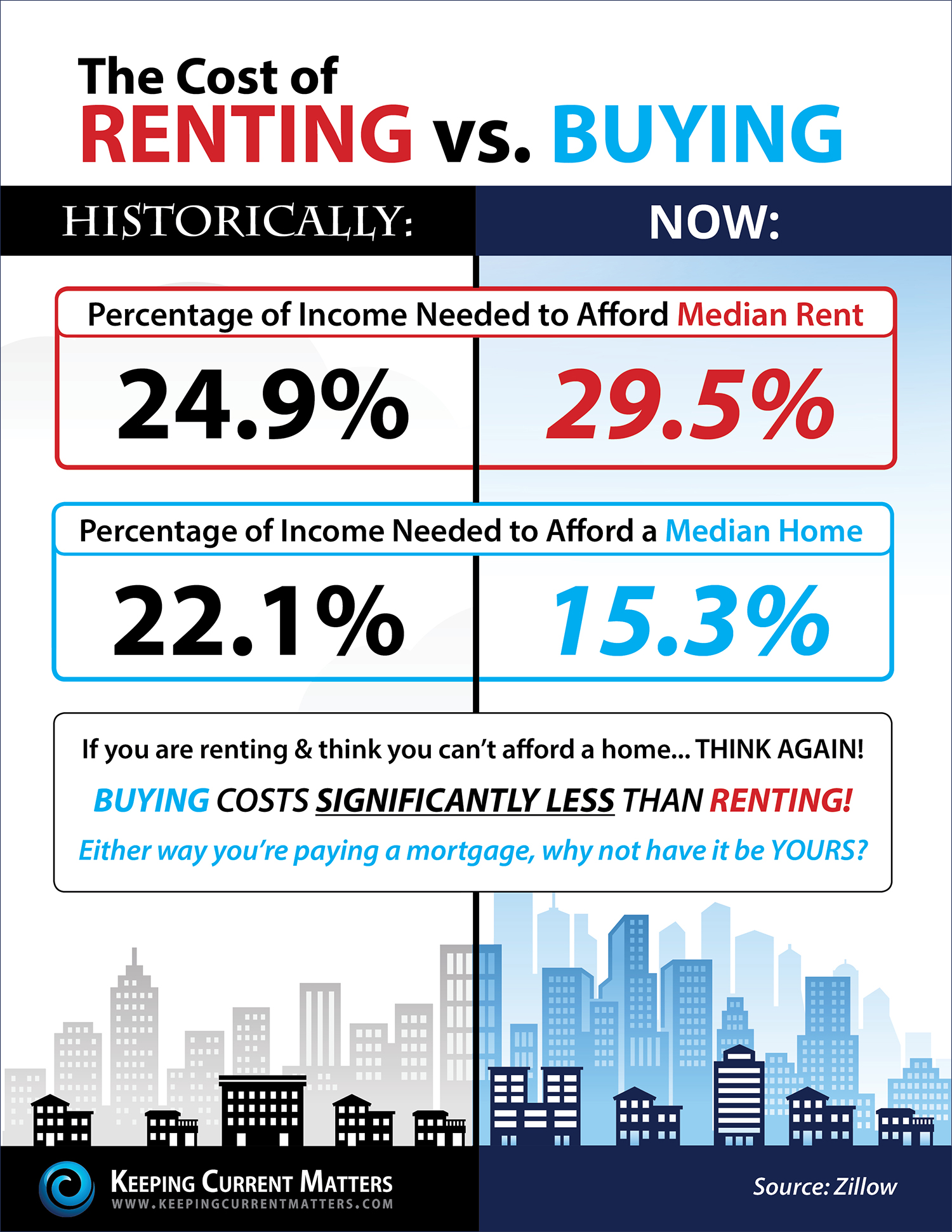

2. To Build Your Personal Wealth

Stop paying your landlord’s mortgage. When you own your home, your mortgage amount is going down and your property value is going up.

No other investment, asset or debt is as misunderstood as a home. A home can be a wonderful and lucrative investment, but like any investment, it needs to be regularly reviewed, maintained and, when appropriate, sold. Even if your home is paid off, you still pay costs for repairs and upkeep, taxes and insurance. But like any investment, if you own it long term, take care of it and sell when the market is right, you stand to make a great gain.

3. Tax Savings (Federal and State)

Under Section 163 of the IRS code, interest on loans used to acquire, construct or improve real estate is deductible on up to a $1,000,000 mortgage.

Interest on loans tied to real estate for any reason is deductible on up to a $100,000 mortgage. For example, interest on the first $100,000 of a home equity line of credit (HELOC) is tax deductible.

Let’s say you make $100,000 per year and rent a home for $1,800 per month. You would have to pay taxes on your entire income of $100,000 when you are renting that home. If you purchase a home with a monthly payment of $1,800, you only have to pay taxes on $78,400 of your annual income because the interest you paid on your mortgage can be used as a tax deduction.

4. Asset Diversification

Unlike with a 401(k) or IRA, when you invest in a home you can live in it while the investment grows.

Owning a home over an extended period of time is usually more lucrative than renting. With good planning and execution, you can learn to minimize the cost of homeownership and maximize the ability to create real wealth. Many small business owners have a home office and can use the home office as a tax deduction while they are earning income. Other homeowners will rent out a bedroom and use the rent to pay down their mortgage and gain equity faster.

5. Forced Savings

Monthly mortgage payments lower your mortgage, essentially creating a forced savings account.

In five years with a $1,800 monthly mortgage payment, you will have paid $29,331 of the principal on your mortgage. That would be money in your pocket if you choose to sell. For this example we use a $345,000 mortgage loan amount at a 4.75 percent interest rate, 4.881 percent APR and use a standard amortization table to come up with the principal pay down.

Guest post by Carl Spiteri, Benchmark Mortgage, News Genius